If you own a North Carolina rental, you can usually depreciate the building over 27.5 years – but not the land. That yearly write-off can lower taxable rental income, and for many owners, it is one of the biggest deductions on the return.

Here’s the short version:

- I start with the building’s cost basis, not the full purchase price

- I exclude land value

- I use the date the property was ready to rent, not the move-in date

- I report depreciation on Schedule E and often Form 4562

- I watch for North Carolina differences on bonus depreciation and Section 179

- I keep records because depreciation can be taxed back at sale through recapture

A few points matter most:

- Residential rental buildings: usually depreciated over 27.5 years

- Land: not depreciable

- Bonus depreciation in NC: 85% add-back, then 20% deduction each year for 5 years

- NC Section 179 cap: $25,000 with a $200,000 investment limit

- Federal passive loss allowance: up to $25,000, with phaseout starting at $100,000 MAGI and ending at $150,000

- Federal recapture rate: up to 25%

- NC flat income tax rate mentioned here: 4.25%

If I had to boil the whole topic down to one line, it would be this: get the basis right, separate repairs from improvements, track federal and NC differences, and keep a clean depreciation schedule from day one.

How to calculate rental real estate depreciation deduction (SL method & mid-month convention)

sbb-itb-aa27f6d

Federal Rules NC Owners Must Apply First

Before North Carolina tax rules kick in, federal depreciation sets the starting line. So if the basis, timing, or forms are off, the state side will be off too.

How to Determine Your Depreciable Basis

Your depreciable basis is the building portion of the purchase price, plus certain closing costs added to basis, such as legal fees and title insurance. Land is not depreciable.

That means you need to split the purchase price between land and building. In most cases, Chapel Hill rental owners use a county assessor allocation or a professional appraisal for that split.

For Durham property owners, this federal step comes first because state reporting begins with the federal number. Start with basis, then move to the recovery period.

Recovery Periods, MACRS, and Placed-in-Service Dates

Residential rental property uses MACRS GDS over 27.5 years. Other assets on the property can follow shorter schedules. Appliances and carpeting often fall into shorter recovery periods, while land improvements like fencing or landscaping generally use a 15-year schedule.

The placed-in-service date is when depreciation begins. In plain English, that means the property is ready and available for rent – not when the first tenant finally signs a lease or moves in.

Residential rental buildings also use the mid-month convention. So even if the property becomes available on the 3rd or the 28th, the IRS treats it as placed in service at the midpoint of that month. It’s one of those tax rules that feels a little odd at first, but it matters when you calculate the first year’s deduction.

How to Report Depreciation on Your Tax Return

Report rental depreciation on Schedule E. File Form 4562 in the first year and again for any new improvement you place in service.

If you missed depreciation in an earlier year, don’t go back and amend old returns just to fix that issue. Instead, use Form 3115 to claim the missed depreciation as a catch-up adjustment.

North Carolina Tax Treatment and Common NC Scenarios

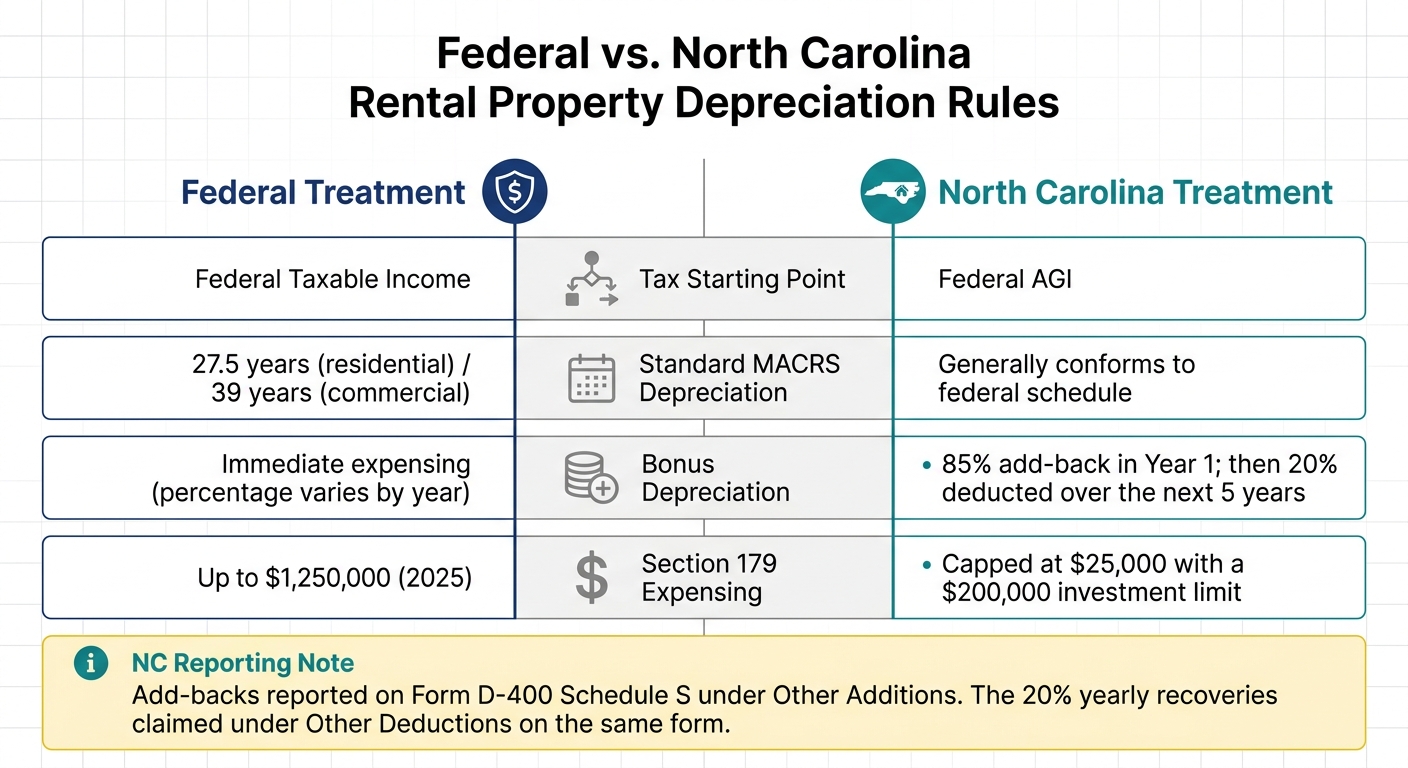

Federal vs. North Carolina Rental Property Depreciation Rules

How NC Income Tax Follows Federal Depreciation

Once your federal depreciation is set, the next step is figuring out how North Carolina handles it.

For residential rentals, North Carolina starts with federal AGI, so the state return will usually track the federal depreciation schedule unless North Carolina calls for an adjustment. In plain English: if you’re using standard MACRS depreciation, you usually won’t need a separate state-level depreciation step.

The main exception is that North Carolina does not fully follow federal rules for bonus depreciation and Section 179 expensing.

For bonus depreciation, North Carolina requires an 85% add-back in the year you take the federal deduction. After that, you recover the add-back by deducting 20% of that amount in each of the next five tax years.

Section 179 works differently too. North Carolina caps Section 179 expensing at $25,000, with a $200,000 investment limit.

You report these add-backs on Form D-400 Schedule S under "Other Additions to Federal Taxable Income." Then you claim the 20% yearly deductions under "Other Deductions" on that same form.

That split is why it helps to keep separate federal and North Carolina depreciation schedules. It saves headaches later, especially when timing differences start to pile up.

Those timing differences matter even more when a rental shows a loss or when the property isn’t used only as a rental.

Passive Loss Limits, Mixed-Use Property, and Short-Term Rentals

This is where state conformity starts to matter more.

If depreciation creates or increases a rental loss, the federal passive loss rules can limit what you can use in the current year. If you meet the active participation rule, you may deduct up to $25,000 in rental losses against non-passive income. That allowance starts to phase out when your modified adjusted gross income, or MAGI, goes over $100,000 and is gone at $150,000.

Mixed-use properties add another layer. If you use a property both personally and as a rental, depreciation has to be prorated based on rental days versus personal-use days. Personal use can also limit how much rental loss you can deduct for the year.

Federal vs. North Carolina Tax Treatment: Side-by-Side Comparison

Here are the main federal and North Carolina differences side by side.

| Item | Federal Treatment | North Carolina Treatment |

|---|---|---|

| Tax Starting Point | Federal taxable income | Federal AGI |

| Standard MACRS Depreciation | 27.5 years (residential) / 39 years (commercial) | Generally conforms |

| Bonus Depreciation | Immediate expensing (percentage varies by year) | 85% add-back in Year 1; 20% deducted over the next 5 years |

| Section 179 Expensing | Up to $1,250,000 for 2025 | Capped at $25,000 with a $200,000 investment limit |

Calculations, Improvements, and Sale Planning

Repairs vs. Capital Improvements: What’s the Difference?

After basis and recovery periods, the next step is deciding whether a cost can be written off now or must be spread out through depreciation later. In plain English: classify each expense before you deduct it.

Here’s the split:

| Category | Definition | Tax Treatment | NC-Relevant Examples |

|---|---|---|---|

| Repairs | Restores property to ordinary working condition without adding major value | Deducted 100% in the current tax year | Interior painting between tenants, patching a roof leak, fixing a broken window, HVAC servicing |

| Capital Improvements | Adds value, extends useful life, or changes how the property is used | Capitalized and depreciated over time, generally over 27.5 years for residential rental property | Roof replacement, flooring upgrades, major HVAC overhauls, rewiring, major plumbing upgrades |

A good rule of thumb: if the work simply gets the property back to normal condition, it’s often a repair. If it makes the property better, lasts longer, or changes its use, it usually falls into the improvement bucket.

How to Calculate Annual Depreciation for an NC Rental

Once you know which costs must be capitalized, the math gets pretty simple. Using the same MACRS rules, a Triangle landlord might run the numbers like this:

| Component | Value / Calculation | Result |

|---|---|---|

| Purchase Price | $350,000 | Starting point |

| Eligible Closing Costs | Title insurance, legal fees, recording fees | + $5,000 |

| Total Cost Basis | Purchase price + closing costs | $355,000 |

| Land Allocation | 20% based on county records | − $71,000 |

| Depreciable Basis | Total basis − land value | $284,000 |

| Annual Building Deduction | $284,000 ÷ 27.5 years | ~$10,327/year |

| Later Improvement (new roof) | $15,000 ÷ 27.5 years | ~$545/year |

That means the building itself produces about $10,327 per year in depreciation. If you later replace the roof for $15,000, that cost does not get folded into the old schedule. It starts its own 27.5-year timeline and adds about $545 per year to your deduction going forward.

Depreciation Recapture and What Happens When You Sell

Depreciation helps while you own the property. But when you sell, part of that tax break can come back around.

The IRS taxes the gain tied to depreciation you claimed at up to 25% federally. That piece is called Unrecaptured Section 1250 gain. North Carolina also taxes that gain at its flat state income tax rate of 4.25%.

This is why recordkeeping matters so much. Hold on to:

- Original purchase documents

- Improvement invoices with dates

- A running depreciation schedule

Without those records, figuring out gain at sale can get messy in a hurry.

If you want to delay capital gains tax and depreciation recapture, a 1031 exchange may help. To do that, you must identify a replacement property within 45 days and close within 180 days.

Recordkeeping, Professional Support, and Key Takeaways

Records NC Landlords Should Keep Year-Round

After you set up depreciation and sale treatment, the next step is simple: keep records that support every figure on your tax return. If the IRS or the North Carolina Department of Revenue reviews your filing, those records do the heavy lifting.

Start with your settlement statement and any appraisal used to divide land value from building value. Then keep your depreciation schedule, invoices for improvements that show the work done and the cost, and any state or contractor paperwork tied to major capital projects.

If the property is mixed-use, keep a personal-use day log so you can back up the rental-day proration. You should also document the placed-in-service date with rehab completion records and the first listing date. Before-and-after photos help too, especially when you need to show that a project was an improvement rather than a repair.

A dedicated bank account for each rental property can make this much easier. So can digital copies of receipts. Small habits like these save a lot of stress later.

How Unicorn Rentals Helps Owners Stay Organized

Keeping up with all of this is a lot easier when property-level reporting is done the same way month after month. For owners who want cleaner records, Unicorn Rentals helps keep depreciation support organized through routine reporting and inspections.

Their monthly financial reporting gives owners a property-by-property view of income and expenses. That helps tax professionals sort out repairs that may be deducted now from capital improvements that must be added to basis. Maintenance coordination logs each service request with dates and descriptions, and regular property inspections build a documented history of the home’s condition. At year-end, owners also get statements that pull the year together for tax filing.

Conclusion: Key Depreciation Rules NC Owners Should Know

Getting expense classification right still matters. Depreciation can cut taxes now, but it also changes gain when you sell. And none of it works well without records that support the numbers.

FAQs

How do I split land value from building value?

To calculate your depreciable basis, subtract the land value from the property’s total purchase price. Land isn’t depreciable, so only the building value counts for depreciation.

Use your property appraisal to split the purchase price between land and building. In the Triangle area, land often accounts for about 22% of the property’s value, which leaves about 78% as the depreciable building basis.

Keep those two numbers clearly separated in your records. That makes tax reporting much easier later.

What if I never claimed depreciation?

If you never claimed depreciation, you usually lose those tax deductions for past years. That’s because the IRS treats depreciation as allowed or allowable. In plain English: even if you didn’t take the write-off, the IRS may still act as if you did.

That matters when you sell the property. Your capital gain can still be figured using the depreciation you were supposed to claim, which may leave you with a bigger tax bill than you expected.

There may be a way to fix missed deductions by filing Form 3115. This can let you catch up on depreciation you didn’t claim. Tax rules here can get messy fast, so it’s smart to talk with a tax professional about your options.

Does NC tax depreciation differently from federal?

Yes. North Carolina generally follows federal MACRS rules, including the 27.5-year recovery period for residential rental property. But it does not fully match federal bonus depreciation or Section 179 treatment.

In many cases, you need to add back 85% of those federal deductions to your North Carolina taxable income. Then you can deduct 20% of that add-back in each of the next five tax years.

State tax rules can shift, so it’s smart to check with a tax professional.