Owning rental property in Raleigh, Durham, or Chapel Hill can be profitable, but managing taxes is crucial. Here’s a quick guide to staying organized and minimizing tax burdens:

- Key Tax Requirements: Federal reporting, North Carolina’s flat 4.75% income tax rate, and varying county property taxes.

- Essential Records: Keep rent rolls, receipts for repairs, utility bills, Form 1098, and contractor W-9s for at least seven years.

- Deductions: Claim expenses like mortgage interest, property taxes, insurance, and repairs. Separate repairs (fully deductible) from improvements (depreciated over time).

- Depreciation: Residential properties depreciate over 27.5 years. Use accurate schedules to avoid issues during property sales.

- Deadlines: Property taxes are due September 1, with an interest-free window until January 5. Business personal property listings are due January 31.

- Quarterly Payments: If you owe $1,000+ in NC state taxes, make quarterly payments to avoid penalties.

Organizing records, reconciling monthly, and leveraging property management fee structures and reports can simplify tax filing. Proper preparation helps reduce tax liabilities and avoid costly mistakes.

Tax Records to Gather Before Filing

Getting your tax documents in order early can save you from headaches, errors, and even audits. The IRS emphasizes this: "If you are audited and cannot provide evidence to support items reported on your tax returns, you may be subject to additional taxes and penalties.". To stay on the safe side, hold onto all relevant records for at least seven years – this applies to audits by both the IRS and NCDOR.

Documents to Collect

Here’s a breakdown of the essential documents landlords in the Triangle area should gather before filing:

| Category | What to Collect |

|---|---|

| Income | Rent rolls, lease agreements, late fee records, and bank statements showing all deposits |

| Operating Expenses | Utility bills, insurance premiums, HOA fees, and property management invoices |

| Maintenance & Repairs | Receipts for repairs, cleaning invoices, landscaping contracts, and pest control bills |

| Financial & Legal | Form 1098 (mortgage interest), property tax statements, and closing disclosures |

| Contractor Payments | W-9 forms from contractors and 1099-NEC forms for those paid above the reporting threshold |

Keep in mind that capital improvements – like major renovations – should be documented separately from routine repairs. Why? Improvements are depreciated over time, while repairs can be deducted in full for the current year. Setting up separate folders for these from the start will save you time and confusion later.

Also, remember that in North Carolina, security deposits are not considered rental income unless they’re forfeited or applied as a final rent payment. Be sure to maintain these in a separate trust account record.

Once you’ve gathered all your documents, proper organization will make reconciliation and audit preparation much smoother.

How to Organize Financial Records

Monthly reconciliation is key. Match your rent ledger to bank deposits every month. This helps catch and fix discrepancies early, avoiding a massive cleanup at the end of the year.

Consider using rental property accounting software. These tools let you assign transactions by property and create accurate profit-and-loss reports. For clarity and audit readiness, maintain separate bank accounts for your rental properties and digitize receipts daily.

"The IRS cares less about your intentions and more about your documentation." – Joe Johnbosco

Taking the time to organize your financial records now will simplify your tax filing process and keep you prepared for any potential audits.

sbb-itb-aa27f6d

Tax Deductions Available to Triangle Area Landlords

Tax deductions can significantly reduce the financial burden of managing rental properties. The IRS allows landlords to deduct expenses that are considered "typical and essential" for maintaining and operating rental properties. What many landlords may not realize is just how extensive this list can be.

Common Deductible Expenses

Many everyday expenses tied to your rental property are deductible. These include:

- Mortgage interest and property taxes

- Insurance premiums

- Advertising costs for finding tenants

- Professional fees, such as property management, legal, and tax preparation services

- Utilities you pay on behalf of tenants

- Mileage for trips related to property repairs or inspections (be sure to keep detailed records)

One key area to understand is the distinction between repairs and improvements. Repairs, like fixing a leaky faucet, repainting, or patching drywall, are fully deductible in the year they’re paid. Improvements, however, are treated differently. Projects like installing a new roof or renovating a kitchen add value or extend the life of the property, so they must be depreciated over several years instead of being deducted all at once. Keeping these categories separate ensures you claim deductions properly and avoid delays.

In addition to these expenses, tracking depreciation is crucial for maximizing your deductions.

How to Track Depreciation

Depreciation is one of the most effective tools landlords can use to reduce their taxable income, but it requires careful attention. Residential rental properties are depreciated over 27.5 years using the straight-line method. However, only the building qualifies for depreciation – the land does not. In the Triangle area, land typically represents about 22% of a property’s value, meaning around 78% of the total purchase price is depreciable.

Here’s an example: A $350,000 rental property would generate approximately $12,700 in annual depreciation deductions. These deductions are reported on Form 4562 and flow through to Schedule E on your federal tax return.

For even greater savings, consider a cost segregation study. This process can reclassify up to 40% of a building’s value into shorter depreciation schedules, allowing for larger deductions in the first year. However, North Carolina applies its own rules. The state requires an 85% bonus depreciation addback, which is then recovered at 17% annually over five years. This differs significantly from federal rules.

| Feature | Federal Treatment | NC State Treatment |

|---|---|---|

| Bonus Depreciation | 100% deductible in Year 1 | 15% deductible in Year 1; 85% addback required |

| Addback Recovery | N/A | 17% of addback deducted annually in Years 2–6 |

| Standard MACRS | 27.5-year schedule | Follows standard schedules |

As with other expenses, maintaining accurate records of depreciation is essential. Keep a separate depreciation schedule to simplify tax filing and to avoid surprises when you sell the property. The IRS will recapture any depreciation you’ve claimed, so having detailed records now can save you from potential headaches later.

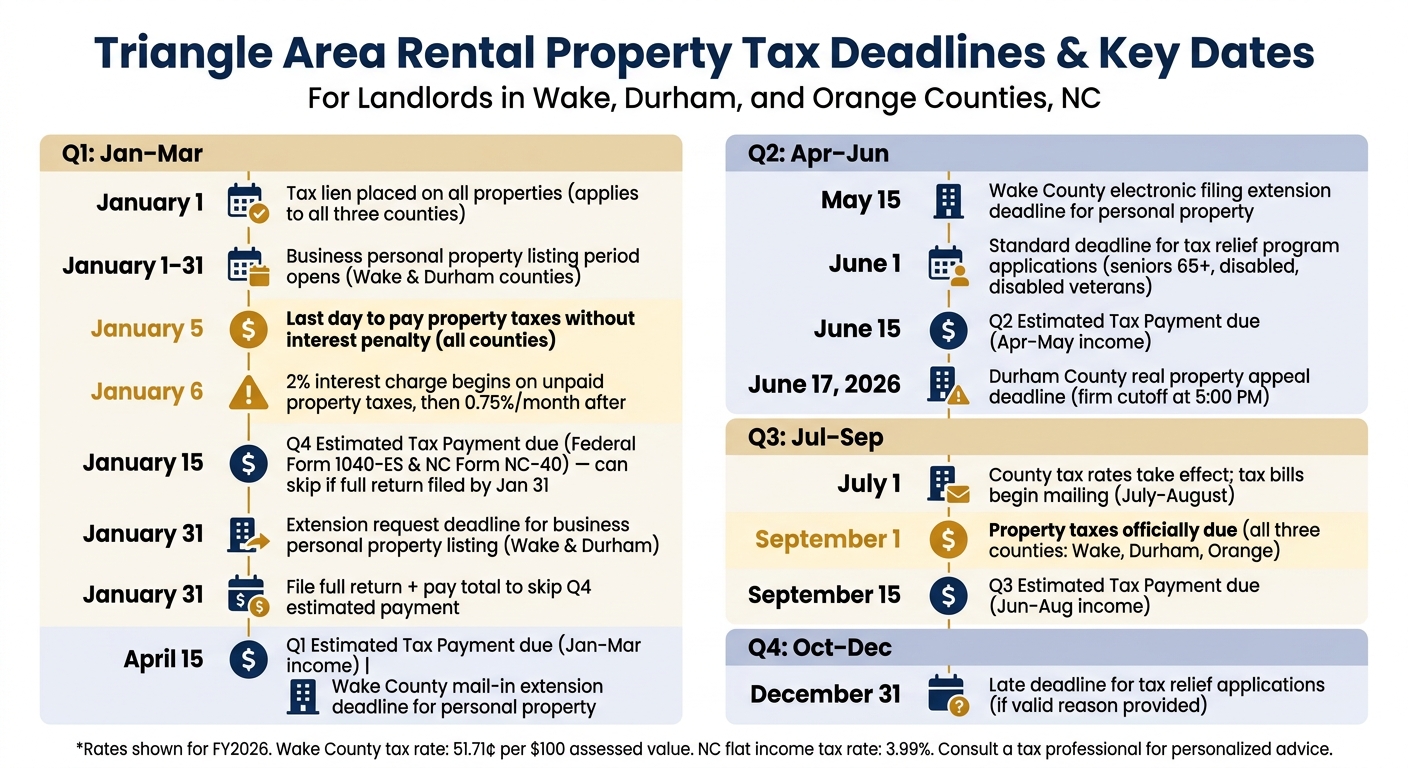

Local Tax Deadlines and Requirements by County

Triangle Area Rental Property Tax Deadlines & Key Dates

Missing a tax deadline can lead to interest charges and penalties. While Wake, Durham, and Orange counties share general similarities in their schedules, there are some important differences to be aware of.

County Property Tax Deadlines

For all three counties, property taxes are due annually on September 1. To avoid interest, payments must be made by January 5. Payments after this date incur a 2% interest charge for the first month, followed by 0.75% monthly for subsequent months.

"Taxpayers can avoid interest and additional costs by paying off their balance by January 5, 2026." – Wake County Tax Administration

For landlords with furnished rental units, Wake and Durham counties require annual business personal property listings. These must be filed between January 1 and January 31, with extensions available upon request by January 31. In Wake County, approved extensions extend the deadline to April 15 for mail-in filings or May 15 for electronic submissions. Durham County extensions generally last through April 15.

Here’s a quick summary of key tax deadlines by county:

| Deadline/Event | Wake County | Durham County |

|---|---|---|

| Listing Period (Personal/Business) | Jan 1 – Jan 31 | Jan 1 – Jan 31 |

| Extension Request Deadline | Jan 31 | Jan 31 |

| Tax Bills Mailed | July | July |

| Taxes Due Date | September 1 | September 1 |

| Interest/Delinquency Date | January 6 | January 6 |

| Real Property Appeal Deadline | Varies (~March 1 Informal) | June 17, 2026 |

Orange County follows North Carolina’s general tax statutes (Chapter 105), with the same September 1 due date and January 5 interest-free window. Tax bills are typically mailed between July and August. For questions, contact Orange County Tax Administration at 919-245-2100.

Additionally, a tax lien is placed on properties on January 1 each year and remains until taxes are paid. If your mortgage includes an escrow account for property taxes, your lender handles the payment. However, since you won’t receive a mailed bill, it’s wise to verify payment through your county’s online portal. Staying on top of deadlines and filing requirements is crucial to avoid penalties.

Checking Assessed Value and Tax Rates

Counties determine tax rates annually, usually in June, with rates taking effect on July 1. For fiscal year 2026, Wake County’s approved tax rate is 51.71 cents per $100 of assessed value. Durham and Orange counties follow a similar process to set their rates.

Each county provides online tools to check property assessments and tax rates:

| County | Online Tool | Phone |

|---|---|---|

| Wake | Wake County Tax Portal | 919-856-5400 |

| Durham | Durham Tax Help Portal | 919-560-0300 |

| Orange | Orange County Tax Administration | 919-245-2100 |

Review details such as square footage and bathroom counts to ensure your property isn’t overassessed. If something seems incorrect, you can file an appeal. Durham County’s 2026 appeal deadline is firm:

"APPEALS MUST BE FILED BY 5:00 P.M. ON June 17, 2026. APPEALS FILED AFTER THIS DATE WILL BE UNTIMELY." – Durham County Tax Administration

Additionally, check if you qualify for any tax relief programs. Seniors (65+), disabled residents, and disabled veterans may be eligible for reductions. For example, Durham County offers a $45,000 Disabled Veteran Exclusion on taxable value. Most programs have a standard application deadline of June 1, though late applications may be accepted through December 31 for valid reasons.

Steps to Complete Before Filing and Payment

Before submitting your tax return, double-check that all your figures are accurate and your records are complete.

Review Ownership Structure and Expenses

Start by confirming your property’s ownership structure. For example, single-member LLCs report income on Schedule E, while active co-owners might qualify as a Qualified Joint Venture (in which case, check the QJV box on Schedule E). If your property is part of a partnership or an S-Corp, make sure the appropriate forms, like Forms 1065 or 1120-S, have already been filed.

Next, categorize your expenses correctly. Immediate repairs, like fixing a leaky faucet, should be recorded as expenses, while larger improvements, like replacing a roof, need to be depreciated over time. Ensure your rental income records are complete, including partial payments, late fees, and prorated rent. Additionally, if you paid any contractor over $600, have a W-9 on file so you can issue a 1099-NEC. For property-related travel, keep a detailed mileage log and calculate costs using the IRS rate of 70¢ per mile for 2025. Also, remember that security deposits held in a trust account at a North Carolina bank are not taxable unless applied to a lease violation or unpaid rent.

Once you’ve confirmed your ownership details and expense records, move on to verifying your quarterly tax payments. If you need assistance with local compliance, consider professional rental property management in Durham.

Verify Quarterly Estimated Tax Payments

If you anticipate owing $1,000 or more in North Carolina state taxes for the year, you’re required to make quarterly estimated tax payments. For the 2026 tax year, the state’s flat income tax rate is set at 3.99%.

Double-check your bank statements and NCDOR eServices confirmations to ensure all payments were made on time. If any payments were late or incomplete, use Form D-422 to calculate any interest owed; the underpayment interest rate is 7% annually through June 30, 2026. As a time-saving tip, if you file your full return and pay the total amount due by January 31, you can skip the Q4 estimated payment otherwise due on January 15. Keep in mind that Form 1040-ES and Form NC-40 have separate payment processes, even though their deadlines are the same.

| Payment Installment | Income Period Covered | Due Date |

|---|---|---|

| Q1 – 1st Installment | January – March 2026 | April 15, 2026 |

| Q2 – 2nd Installment | April – May 2026 | June 15, 2026 |

| Q3 – 3rd Installment | June – August 2026 | September 15, 2026 |

| Q4 – 4th Installment | September – December 2026 | January 15, 2027 |

Using Property Manager Reports to Simplify Tax Filing

Once you’ve verified your quarterly payments and categorized expenses, the next step is gathering property manager reports. These reports are a goldmine of organized data, saving you time and effort during tax preparation. Essentially, they connect your financial records with the tax filing process, ensuring everything stays consistent and accurate.

Reports to Request from Your Property Manager

To make tax season less stressful, ask your property manager for a property-level Profit and Loss (P&L) statement and a rent roll. These two documents are crucial for completing Schedule E. The P&L provides a detailed breakdown of income – like rent, late fees, and parking – against all operating expenses. Meanwhile, the rent roll logs tenant payment histories, including dates and fees, helping you verify your gross rental income.

Additionally, there are two other key reports you should request:

- A maintenance and repair records report: This helps differentiate between repairs (deductible expenses) and improvements (capitalized costs).

- A security deposit ledger: This confirms which deposits are held in trust as liabilities and which were applied to damages or unpaid rent. This distinction is vital because it affects what you report as taxable income.

These reports act as an extension of your financial records, making it easier to ensure everything aligns when it’s time to file taxes.

| Report Type | Key Data Included | Tax Purpose |

|---|---|---|

| Income Statement (P&L) | Total rent, late fees, itemized expenses | Calculates net taxable income for Schedule E |

| Rent Roll | Tenant names, lease terms, payment history | Verifies rental income during an audit |

| Owner Statement | Cash flow, management fees, net disbursements | Tracks deductible management costs |

| Security Deposit Ledger | Deposits held in trust, itemized deductions | Ensures deposits aren’t taxed as income |

Tip: Cross-check any depreciation details provided by your property manager with your prior records to avoid discrepancies.

How Professional Financial Reporting Helps at Tax Time

Professional financial reports do more than just present raw numbers – they seamlessly integrate with your tax documentation. For example, landlords working with property managers who provide structured monthly reports can save 12–15 hours of bookkeeping each month. That saved time becomes even more valuable during tax season, when poor organization often leads to missed deductions.

Take Unicorn Rentals as an example. They include financial reporting in all their property management plans for Triangle area properties. Their reports are designed to match IRS Schedule E categories, which means expenses like management fees, repairs, and property taxes are already sorted into the correct categories before you even hand them to your accountant. For landlords managing multiple properties, their consolidated portfolio reports provide a big-picture view, helping you spot trends and ensure no details are overlooked.

"Monthly reconciliation prevents the accumulation of errors that become disasters at tax time." – Madras Accountancy

One smart move? Ask your property manager to clearly separate capital improvements from routine repairs in their year-end summary. Misclassifying these is a common red flag for IRS audits. Once you’ve gathered all the necessary reports, take time for a final review to ensure your documentation is complete before filing.

Conclusion: Staying on Top of Rental Property Taxes

Managing rental property taxes in the Triangle area – covering Raleigh, Durham, and Chapel Hill – requires attention to several key areas: understanding county-specific tax rates, making quarterly estimated payments, following depreciation schedules, and adhering to North Carolina’s compliance rules. Staying organized and maintaining accurate documentation can help you minimize tax liabilities and reduce the risk of audits.

Two habits can simplify this process: conducting monthly reconciliations and keeping detailed records for at least seven years. Catching issues like duplicate insurance payments or miscategorized expenses early is far easier than unraveling them during tax season. For those with complex ownership structures or multiple properties, working with a professional can make all the difference. Plus, fees for CPAs and property management services are fully deductible, which can ease the financial burden.

If you’re partnered with a property manager like Unicorn Rentals, which serves the Raleigh, Durham, and Chapel Hill areas, you’ll benefit from financial reports aligned with IRS Schedule E categories. This alignment streamlines your preparation, saving both you and your accountant valuable time.

The key to a stress-free tax season is consistency. By adopting small, regular habits throughout the year, you can simplify the process and ensure you’re maximizing your deductions.

FAQs

How do I know if something is a repair or an improvement?

The main distinction comes down to their purpose and effect. Repairs are about bringing a property back to its original state without increasing its value or lifespan – think fixing a cracked window. On the other hand, improvements enhance the property by adding value, extending its life, or preparing it for a different use – like installing energy-efficient windows. To ensure accurate classification and maximize deductions, keep detailed records, including invoices and photos, of all expenses.

What rental property records should I keep in case of an audit?

Keeping thorough records of your rental property is crucial. Track everything: rental income, including payment dates and amounts, as well as expenses like repairs, improvements, and other deductible costs. Keep receipts, invoices, and documentation for these expenses.

Additionally, maintain copies of legal documents such as deeds, contracts, insurance policies, permits, security deposit records, tenant information, and details of any capital improvements made to the property. These records should be stored securely for at least seven years, ensuring you’re prepared in case of an audit or legal inquiry.

Do I have to pay quarterly estimated taxes in North Carolina?

If you owe $1,000 or more in North Carolina state taxes after accounting for withholding and credits, you’re required to make quarterly estimated tax payments. Make sure to evaluate your tax obligations carefully to avoid penalties and ensure compliance.